If you are thinking of setting up a business, or if you already operate as a sole trader, you may be asking the question, when should I incorporate my business? If incorporating your business is on your mind, the next question might be when should I incorporate my business?

The answer to these questions will affect the way in which you run your business and ultimately, what taxes you pay, and when you pay them. This is not a decision that should be taken lightly.

Operating as a sole trader – should I incorporate my business?

If you run your business as a sole trader, there is no distinction for tax purposes between you and your business. Any profits that you make from running your business are taken into account in working out your overall tax liability for the tax year. The rate at which you pay tax depends on your total taxable income for the year, not just on the level of your business profits.

If you make a loss, relief may be available for that loss. The reliefs that are available for that loss will depend on whether you use the cash basis or the traditional accruals basis to work out your profit or loss.

If your profits from all sources of self-employment are £1,000 or less, you benefit from the trading allowance and do not need to tell HMRC or pay any tax on them. Above this level, you can deduct the £1,000 allowance instead of actual expenses to arrive at your taxable profit where this is beneficial.

From 2024/25 onwards you will be taxed on the profits for the tax year, with 2023/24 being a transitional year.

If you start your business in 2023/24 or 2024/25, it will be advantageous to pick a 31 March or 5 April year end to make life easier under the tax year basis and remove the need to apportion the profits from two accounting period to arrive at the taxable profit for the tax year. If you currently do not have a 31 March or 5 April accounting date, you may wish to consider changing your accounting date.

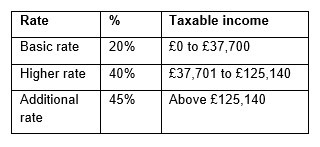

For 2024/25, the basic personal allowance is £12,570. Income tax is charged on taxable income as follows:

Scottish taxpayers pay income tax at the Scottish income tax rates. You will also pay Class 4 National Insurance if your profits are above £12,570. For 2024/25, Class 4 National Insurance is payable at the rate of 6% on profits between £12,570 and £50,270 and at the rate of 2% on profits in excess of £50,270.

If your profits are more than £12,570, no Class 2 National Insurance will be payable. If your profits are between £6,725 and £12,570, you are treated as if you have paid Class 2 contributions at a zero rate, providing a qualifying year without actually having to pay Class 2 contributions. If you have profits of below £6,725, you must opt to pay Class 2 contributions voluntary at a rate of £3.45 per week to preserve your contributions record.

Operating as a limited company – should I incorporate my business?

If you choose to operate your business as a limited company, the first point to note is that the company is a separate legal identity and pays tax in its own right.

The company must pay corporation tax on its profits. Unlike an individual, there is no tax-free allowance for a company; corporation tax is payable from the first pound of taxable profit.

From 1 April 2023, the rate at which corporation tax is payable depends on your profits.

If profits are less than the lower profits limit, set at £50,000 for a standalone company, the corporation tax rate is 19%.

However, if your taxable profits are more than the upper profits limit, set at £250,000 for a standalone company, you will pay tax at 25%. Between these limits, the tax charge is initially calculated at 25%, but is reduced for marginal relief, so that the effective rate is between 19% and 25%.

The limits of £50,000 and £250,000 are proportionately reduced if you have associated companies or prepare accounts for a period of less than 12 months.

If you operate your business as a company and you want to use your profits outside of the company, for example, to meet your living expenses, you will need to take the profits out of the company, and depending on the route chosen, this may incur additional tax and possibly National Insurance liabilities.

A popular and tax-efficient strategy is to pay a salary at the personal allowance and primary threshold for Class 1 National Insurance purposes (set at £12,570 for 2024/25). Any further profits can be extracted as bonuses or dividends.

Whilst there is no National Insurance payable on dividends and also that the dividend tax rates are lower than the rates of income tax, it is often no longer the case that dividends are more tax efficient than bonuses. For 2024/25, the first £500 of dividend income is tax-free.

Thereafter, dividends (which are treated as the top slice of income) are taxed at:

• 8.75% to the extent that they fall within the basic rate band,

• 33.75% to the extent that they fall within the higher rate band, and

• 39.35% to the extent that they fall within the additional rate band.

Dividends are paid out of the company’s retained profits that have already suffered corporation tax. Consequently, companies that have exhausted their reserves of retained profits can no longer make dividend payments to shareholders.

Should I incorporate my business?

At first sight, it may seem beneficial to operate as a limited company if the company will pay corporation tax at the rate 19% as lower than even the basic rate of income tax. Incorporation may also be beneficial if the company is paying corporation tax at 25% as this is considerably lower than the additional rate of income tax at 45%.

However, this is not the full picture – a company has no tax-free allowance, and further tax and National Insurance may be payable if you extract the profits from the company for personal use.

The increase in the corporation tax rates from April 2023, the increase in the dividend tax rates from 6 April 2022 and the reduction in the dividend allowance from 6 April 2023 mean incorporation is less attractive than it once was. Depending on personal circumstances and the level of profits, these changes may have the effect of swinging the pendulum away from incorporation.

The most tax-efficient option will depend on personal circumstances and will be affected by the level of profits that your business makes and also any other income that you may have.

There is no substitute for crunching the numbers; this is essential to assess which is the most tax-efficient option for you.

It is also important to plan ahead. While incorporation relief is available if you incorporate your business in exchange for shares, there is currently no relief if you disincorporate, and moving between structures can in itself trigger tax bills.

Limiting liability – Should I incorporate my business?

Aside from the tax and National Insurance issues in the previous sections of this update, business owners should consider their personal liability should their business fail.

In a nut-shell, if you are self-employed (whether sole trader or in a regular partnership structure) if your business becomes insolvent you may become personally liable for business debts not covered by business assets.

It is possible to cover this risk by converting to a Limited Liability Partnership, but this will not change your tax status.

Incorporation as a Private Limited Company is probably your best option if commercial risks are a significant factor. This may be so even if the tax benefits are marginal.

RPGCC’s Tax and business advisers can help…

The shift towards a higher company tax regime combined with a less generous dividend allowances and higher tax rates for dividends complicates the issues to be considered when deciding on a self-employed or incorporated business structure.

Are you asking yourself “should I incorporate my business” now might be the time to seek professional advice and get the answers you need. RPGCC can help you work out what is the most tax efficient, and risk averse structure for your business.

If you would like to speak to a member of the RPGCC team about how to incorporate your business or if after reading this article you have further questions, please contact us on 020 7870 9050.