What is an Associated Company?

If you are within the scope of corporation tax, you may be aware that the rules changed from 1 April 2023. From that date, a company will pay corporation tax at the small profits rate of 19% if its profits are below the lower profits limit, whereas a company will pay corporation tax at the main rate of 25% if its profits exceed the upper limit. Where profits fall between the two limits, corporation tax is payable at the rate of 25%, as reduced by marginal relief (the marginal rate in this band is 26.5%).

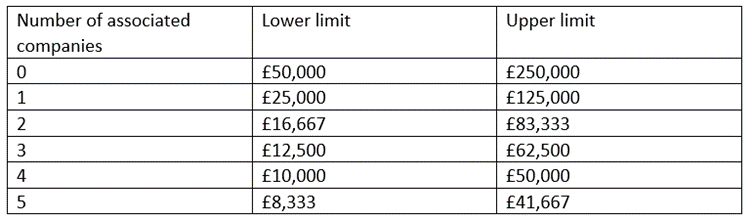

The limits

For a 12-month accounting period, the lower limit for a company with no associated companies is £50,000 and the upper limit is £250,000. Where a company has one or more associated companies, these limits are divided by the number of associated companies plus one.

The following table shows the limits that apply for a 12-month accounting period where a company has between 0 and 5 associated companies.

The limits are proportionately reduced where the accounting period is less than 12 months.

Meaning of ‘associated company’

A new definition of ‘associated company’ applies for the purposes of working out the upper and lower limits from 1 April 2023 onwards. You will need to use this definition to work out whether, and if so, how many, associated companies you have in order to determine the lower limit and upper limit that apply to you.

A company is associated with another company in an accounting period if it meets the definition of an associated company for any part of the accounting period. The companies do not need to be associated for the whole accounting period to be considered. Nor do the companies need to be UK resident to be considered an associate.

A company is an associated company of another at any time when:

• one of the two has control of the other; or

• both are under the control of the same person.

Where a company has two or more associated companies, each company is counted to determine the number of associates that the company has, even if the companies are associated for different parts of the accounting period. For example, if a company with a 12-month accounting period to 31 March 2024 is associated with one company from 1 April 2023 to 31 May 2023 and with another company from 1 January 2024 to 31 March 2024, the company has two associated companies, even though the periods for which they are associated do not overlap.

However, a company is ignored in determining the number of associates that a company has if:

• it has not continued a trade or business at any time in the accounting period; or

• if it was an associated company for only part of the accounting period and has not continued a trade or any business during that part of the accounting period.

A company which carries on a business of making investments in an accounting period and which does not continue a trade, has at least one 51% subsidiary and is a passive company is treated as not carrying on a business in an accounting period (and can be ignored when counting associated companies).

Meaning of ‘control’

The definition of ‘control’ is that which applies for the purposes of the close companies rules.

Under this definition, a person is treated as having control over a company if that person exercises, is able to exercise or is entitled to acquire, direct or indirect control of the company’s affairs. The control test is concerned solely with the shareholders’ ‘share’ power or voting power and loan capital. Control by directors or management is irrelevant.

In particular, a person is treated as having control of a company if the person possesses or is entitled to acquire:

• the greater part of the share capital or issued share capital of the company; or

• the greater part of the voting power in the company; or

• so much of the issued share capital of the company as would, on the assumption that the whole of the income of the company were distributed among participators, entitle that person to receive the greater amount so distributed; or

• such rights as would entitle that person, in the event of the winding up of the company or in any other circumstances, to receive the greater part of the assets of the company which would then be available for distribution among the participators.

If two or more people together satisfy any of the above tests, then they are treated as having control of the company.

Attribution of rights and powers of others

In determining whether a person has control over a company, you must also consider anything that are person is entitled to acquire at a future date and anything which the person will at a future date be entitled to acquire.

If a person possesses any rights and powers on behalf of another person or may be required to exercise any rights or powers on another person’s direction or behalf, those rights and powers are attributed to that other person.

The following rights and powers are also attributed to a person:

• all the rights and powers of a company which a person has, or the person and an associate have, control;

• all the rights and powers of two or more such companies;

• all the rights and powers of an associate of the person; and

• all the rights and powers of two or more associates of the person.

In deciding whether two or more companies are associated, control is determined by considering:

• The direct rights of an individual: these are the rights of ownership personal to the individual.

• The indirect rights of an individual: these are rights of the individual’s associates attributed to them according to whether the substantial commercial interdependence test applies.

An individual’s associates include:

• Spouses (and civil partners), but not if divorced.

• Blood relatives.

• An individual beneficiary will be associated with a trustee or settlor of a trust.

Exception: Substantial commercial interdependence

Where the relationship between two companies is not one of substantial commercial interdependence it is not necessary to attribute the indirect rights of an individual’s associates in order to determine control.

Commercial Interdependence is determined by either financial interdependence, economic interdependence or organisational interdependence.

Where there is no substantial commercial interdependence the only companies that will be treated as being associated are the companies under the direct control of the same individual or group of individuals.

Fixed rate preference shares

In determining whether a company is under the control of another company, fixed rate preference shares are ignored if the company holding them is not a close company, takes no part in the management or conduct of the company that issued the shares or in the management or conduct of its business and subscribed for the shares in the ordinary course of a business which includes the provision of finance.

We can help

The full definition of an associated company can be found on the HMRC website as part of their official company taxation manual. The team here at RPGCC can help you work out whether you have any associated companies and calculate the lower limit and upper limit that will apply to you. If you would like to speak to a member of our team please contact us on 020 7870 9050.